Vikram Solar Q4 and FY26 Results Conference Call: ₹4,802 Cr Revenue

Vikram Solar’s Q4 and FY 2026 earnings conference call, held on May 8, 2026, highlighted a landmark year of record-breaking financial growth and a decisive shift toward becoming a fully integrated renewable energy major.

Below is the summary and key highlights from the call.

Contents

1. Financial Performance (FY 2026)

The company delivered a “multi-bagger” financial performance, with profitability surging far ahead of revenue growth.

-

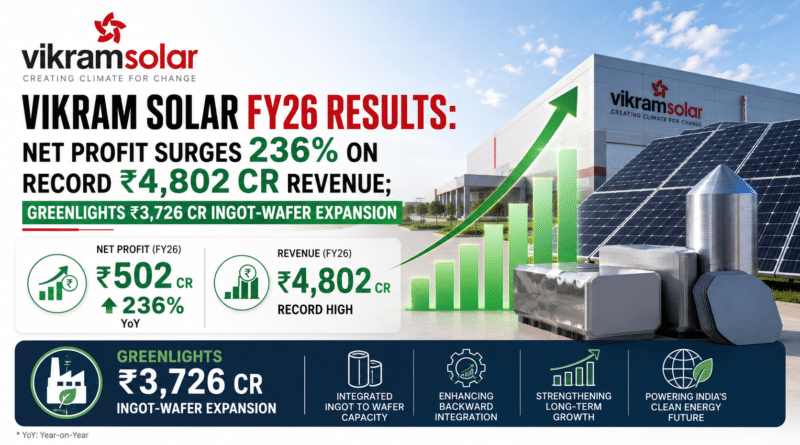

Revenue: ₹4,802 Crore (↑ 40% YoY).

-

EBITDA: ₹917 Crore (↑ 86% YoY).

-

Net Profit (PAT): ₹470 Crore (↑ 236% YoY).

-

Operating Margins: EBITDA margin expanded to 19% (up from 14% in FY25), driven by scale and better operational discipline.

-

Q4 Specifics: Record quarterly revenue of ₹1,453 Crore (the highest in the company’s history).

2. Operational Excellence & Production

Management emphasized that “scale and execution” were the primary drivers of the year’s success.

-

Record Production: Achieved highest-ever quarterly production of 971 MW in Q4 FY26.

-

Annual Volume: Total production surged 150% YoY to 3,220 MW.

-

Capacity Utilization: Achieved a healthy 75% effective utilization for the full year, even with the new Vallam plant in its ramp-up phase.

-

Global Milestone: The company crossed 10 GW in cumulative global deployments (equivalent to 25 million modules).

3. Strategic “Backward Integration” Roadmap

The most critical part of the call focused on the company’s transition from a component provider to a fully integrated manufacturer to combat import reliance.

-

Wafer-Ingot Facility (New Approval): The Board approved a ₹3,726 Crore CAPEX for a 6 GW integrated wafer and ingot facility at Gangaikondan, Tamil Nadu. This is Phase 1 of a 12 GW roadmap for FY30.

-

Solar Cells: The 9 GW cell plant is on track for “first cell-out” in December 2026, which will provide 70% backward integration for their module business.

-

Module Capacity: Targeting 15.5 GW of integrated module capacity by FY30.

4. Order Book & Market Mix

-

Strong Backlog: The order book stood at 8.2 GW as of March 31, 2026.

-

Record Bookings: Secured 1.9 GW of new orders in Q4 alone.

-

De-risking: Customer concentration risk was significantly reduced; the share of the top 5 clients dropped from 80% to 47%, indicating a much broader, deeper revenue base.

-

Pass-Through Protection: Approximately 80% of the order book carries “cell price pass-through” clauses, protecting margins from raw material volatility.

5. Leadership & New Platforms

-

New CEO: Sameer Nagpal was formally introduced as the new CEO. He emphasized a mandate for “operational discipline and strengthening execution rigor.”

-

BESS (Battery Energy Storage): Launched the flagship battery brand “VION” under VSL Powerhive.

-

Target: 15 GWh BESS capacity by FY30.

-

Timeline: 5 GWh cell-to-pack facility to commission by March 2027

-

6. Management Outlook

Chairman Gyanesh Chaudhary concluded that Vikram Solar is entering a “defining moment” where “Energy Independence is Sovereignty.” The company’s long-term goal is to control the entire value chain—from raw ingot to finished battery-backed solar systems—positioning it as one of the largest integrated solar platforms globally by 2030.

Vikram Solar Limited: Q4 and FY 2026 Earnings Conference Call

Date: May 8, 2026 Moderator: Ms. Sheetal Khanduja, Go India Advisors

Management Participants:

-

Mr. Gyanesh Chaudhary: Chairman and Managing Director

-

Mr. Sameer Nagpal: Chief Executive Officer

-

Mr. Ranjan Jindal: Chief Financial Officer

-

Ms. Reenal Shah: General Manager, Corporate Finance

Introductory Remarks

Moderator: Good morning, everyone, and welcome to Vikram Solar’s earnings call to discuss Q4 and FY 2026 results. We have the senior management team with us today. I now request Mr. Chaudhary to take us through the business outlook and financial highlights.

Mr. Gyanesh Chaudhary (CMD): Thank you, Sheetal. Good morning, everyone. FY 2026 has been a year of great significance for us. For import-led economies like India, energy dependence is now a structural risk. Solar uniquely sits outside of geopolitical disruptions. Energy independence is sovereignty.

India is currently the world’s third-largest solar market by annual additions and is projected to move to second within the calendar year. We are building for the coming decade. I am pleased to welcome Sameer Nagpal as our Chief Executive Officer. Sameer brings over 35 years of leadership experience and his mandate is driving operational discipline and strengthening execution rigor.

I now turn to our backward integration roadmap. Vikram Solar will capture the value chain upstream and convert India’s solar surge into enduring profitability. Our strategy moves in three stages: modules first, then cell, then wafer and ingot. By the end of this roadmap, Vikram Solar will be fully integrated from ingot to module.

Regarding Battery Energy Storage (BESS), it is the piece that converts intermittent solar into dispatchable power. Our target is 15 GWh of BESS capacity by FY 2030, positioning us as one of the largest integrated solar platforms. I now hand over to our CEO, Sameer.

Mr. Sameer Nagpal (CEO): Thank you, GC. Q4 is the clearest expression of the momentum we are carrying into FY 2027. We delivered our highest-ever quarterly production of approximately 1 GW, secured our highest-ever order booking of 1.9 GW, and recorded record quarterly revenue of over ₹1,450 crore.

India added 45 GW of solar in FY 2026, nearly double the 24 GW target. We have reached a pivotal maturity phase where policy certainty is aligning for a vigorous push for backward integration. The cell-level mandate effective June 2026 is a critical milestone that forces a shift from assembly to true manufacturing.

Regarding project execution, we took the 5 GW Vallam facility from ideation to commissioning in under nine months. We are now replicating that playbook at Gangaikondan. The 6 GW module facility there is in the final stretch, with first output on track for June 2026. On the 9 GW TOPCon cell facility, we anticipate first cell-out in December 2026 or early January 2027. We have placed orders for cell equipment belonging to the latest TOPCon+ generation.

In three years, Vikram Solar will be operating its 6 GW wafer-ingot facility (scaling to 12 GW by FY 2030), its 12 GW cell facility, and 15.5 GW of fully integrated module capacity. I hand this over to Ranjan for the financial walkthrough.

Mr. Ranjan Jindal (CFO): Thank you, Sameer. During the year, the company delivered record revenue of ₹4,800 crore, up 40% year-on-year. Sales volume reached 3.3 GW, a 76% increase. EBITDA for the year was ₹917 crore with margins expanding to 19%. Profit after tax was ₹478 crore, representing a 10% PAT margin.

Q4 revenue was ₹1,450 crore, up 31% sequentially, with EBITDA at ₹235 crore (16% margin) and PAT at ₹110 crore. Our net working capital cycle compressed from 82 days in FY 2025 to 44 days in FY 2026. Importantly, the company carries no long-term debt, with a net debt-to-equity ratio of 0.03.

Our order book stands at 8.2 GW as of March 31, 2026. The mix is anchored by IPPs at 69%, C&I at 13%, and Government/EPC at 18%. Approximately 80% of our order book carries cell price pass-through clauses, insulating our P&L from input volatility.

Regarding our integration roadmap, the 9 GW TOPCon cell plant is on track for the first cell in December 2026. The 6 GW backward-integrated wafer and ingot facility was approved by the board yesterday with an outlay of approximately ₹3,700 crore and commissioning in FY 2029. This addition turns Gangaikondan into a single integrated campus with zero transport costs between fabs.

For BESS, a 5 GWh cell-to-pack facility is scheduled to commission by March 2027, followed by a 7.5 GWh battery cell manufacturing facility in February 2029.

Question & Answer Session

Sahil Sheth (Anand Rathi): Regarding the 2 GW domestic cell procurement from Jupiter International, when will we see DCR modules rolling out? Ranjan Jindal: The agreement is phased to take care of the DCR demand which kicks in post the June 2026 deadline. Sahil Sheth: Regarding the 9 GW cell facility, what is the CAPEX differential since you are now procuring machinery directly from China vs. Thailand? Ranjan Jindal: It was a 10% cost increase; total cell CAPEX for the 9 GW is ₹5,400 crore. Most will be deployed in the current year.

Ankur Gulati (Janus Capital): Any thoughts on forward or horizontal integration? Sameer Nagpal: We are focused on backward integration for modules and expanding into BESS. We aren’t thinking beyond that currently.

Anuj Kapadia (Taurus Mutual Fund): What was the raw material cost movement in Q4? Ranjan Jindal: We saw some increases in crude oil impacting EVA and aluminum frames, but that was partly compensated by a fall in cell prices. We maintain an inventory of 30 days at the plant level.

Kaushik Joshi (ICICI Securities): Does the 1.9 GW order inflow include distribution? Sameer Nagpal: No, we have taken distribution out of the order booking format. Most distribution was Non-DCR; as the mandate moves to DCR, we have changed the format to spot buying by distributors. Kaushik Joshi: Has the 6 GW capacity addition been done? Sameer Nagpal: It remains on track to commission within June.

Akshay (UBS): Regarding BESS, you highlighted DCR mandates targeting 60% localization. How much can be achieved through assembly? Reenal Shah: Assembly of the cell-to-pack facility is scheduled for March 2027. Localization mandates are a positive movement and we anticipate an Approved List of Battery Manufacturers (ALBM) policy similar to ALMM.

Sagar Parekh (Renaissance Asset Managers): Regarding the 2 GW procurement, what is the spread? Ranjan Jindal: I can’t share specifics, but it maintains the company’s EBITDA per watt expectations. Sagar Parekh: You removed 1 GW of distribution and 1.5 GW of C&I from the order book. How confident are you in gaining that back? Sameer Nagpal: As the mandate moves to DCR, we want to optimize margins on the DCR portfolio because of limited supply. Our distribution channel is very robust with over 110 distributors and 550+ dealers.

Bala Murali Krishna (Omanus Investment): Regarding debt levels, you previously planned ₹3,500 crore by end of FY 2027. Ranjan Jindal: Closing debt for March 2027 is now estimated at ₹3,200 crore. For FY 2028, with the wafer/ingot CAPEX, we expect it to be around ₹6,500 crore. Interest for projects in the CAPEX phase is capitalized and not charged to the P&L.

Deepak Purswani (Swan Investments): With module capacity reaching 15.5 GW, what is the sales strategy? Ranjan Jindal: We expect to produce about 8 GW in FY 2027 (2 GW DCR, 6 GW Non-DCR). Our domestic order book is 7.2 GW, leaving 1.2 GW to be filled by Non-DCR “grandfathered” projects.

Bhavna Jain (Abakkus Capital): What is the EBITDA per watt peak without DCR modules? Ranjan Jindal: Q4 was ₹2.35. For the full year, Non-DCR should deliver ₹1.75 to ₹2.00 on an average basis. Bhavna Jain: What is the expectation after cell integration? Ranjan Jindal: We believe FY 2028 should deliver about ₹5 per watt peak with full integration. Bhavna Jain: What are the utilization targets? Ranjan Jindal: For modules, 65-70% on a nameplate basis; for cells, 70-75%.

Nidhi Shah (ICICI Securities): You previously planned 3 GW in the US; has that been scrapped? Gyanesh Chaudhary: We have done the groundwork, but India looks infinitely more attractive currently because of the supply chain requirements and lack of skilled power in the US. Nidhi Shah: Since November, India’s exports to the US have zeroed out. How secure is your 1 GW US order book? Gyanesh Chaudhary: These are long-term conversations with reputed IPPs. We are working on a traceable, compliant supply chain from North Africa which does not have prohibitive tariffs.

Dhaval (Arihant Capital): What is the growth guidance? Ranjan Jindal: We plan to deliver 7.5 to 8 GW in FY 2027 and an EBITDA range of ₹1,500 to ₹1,600 crore.

Shashank Jha (Individual Investor): Does the BESS have a multiplication factor like solar (1 MW AC needs 1.5 MW DC)? Reenal Shah: It depends on the storage duration (2 to 6 hours). For 80 GW of solar with storage, you would need roughly 320 GWh of DC blocks.

Vishad Kabra (Holani Venture Capital): How much can you pass on rising silver costs? Ranjan Jindal: Current MSAs allow us to pass through 80% of cell and currency costs. Going forward with our own cells and wafers, we will have to see how the market pans out.

Moderator: That was the last question. I hand over to management for closing comments.

Mr. Ranjan Jindal (CFO): Thank you all for joining. We remain committed to keeping you informed. Please feel free to reach out to us or Go India Advisors for further queries.