Emmvee Photovoltaic Power Limited – Q3 & 9M FY26 Results Summary (Investor View)

Contents

Emmvee Photovoltaic Power Limited – Q3 & 9M FY26 Results

Emmvee Photovoltaic Power Limited has delivered an exceptionally strong performance in Q3 FY26 and the first nine months of FY26, firmly establishing itself as one of India’s fastest-growing and most profitable solar manufacturing companies. The latest results highlight sharp revenue growth, expanding margins, a robust order book, and a debt-free balance sheet—an enviable combination in the capital-intensive renewable energy space.

📊 Financial Performance: Strong Across All Metrics

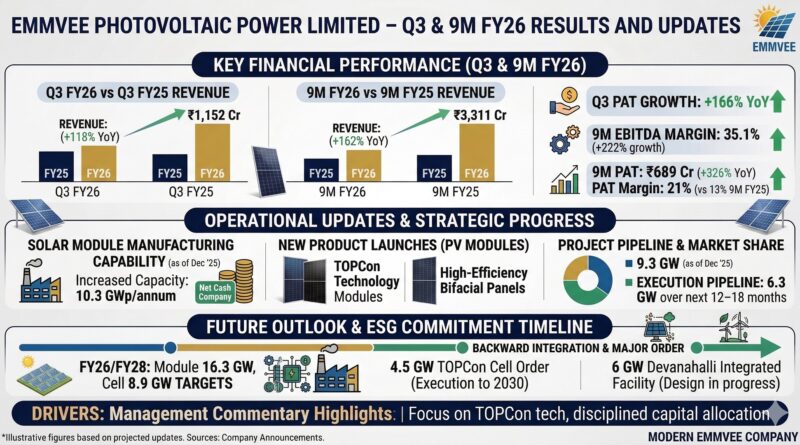

Q3 FY26 Performance (YoY Comparison)

Emmvee reported Revenue from Operations of ₹1,152 crore, registering a massive 118% year-on-year growth. This sharp rise was driven by higher capacity utilisation, new module lines, and strong demand for high-efficiency solar products.

-

EBITDA: ₹413 crore (+105% YoY)

-

EBITDA Margin: 35.9%, reflecting excellent operating efficiency

-

Profit After Tax (PAT): ₹263 crore (+166% YoY)

-

PAT Margin: 23%, up from 18% in Q3 FY25

The company has successfully translated scale into profitability, a key differentiator versus many peers.

9M FY26 Performance (YoY Comparison)

For the first nine months of FY26, growth was even more impressive:

-

Revenue: ₹3,311 crore (+162% YoY)

-

EBITDA: ₹1,163 crore (+222% YoY)

-

PAT: ₹689 crore (+326% YoY)

-

PAT Margin: 21% (vs 13% in 9M FY25)

👉 This clearly indicates operating leverage, with profits growing faster than revenues.

⚙️ Capacity Expansion: Scaling with Discipline

Emmvee commissioned a new 2.5 GW solar module manufacturing line at its Sulibele facility in December 2025. With this addition:

-

Total module capacity: 10.3 GW (as of Dec 2025)

-

FY28 targets:

-

16.3 GW module capacity

-

8.9 GW cell capacity

-

The company is scaling aggressively but with a clear roadmap and visibility.

📦 Order Book & Growth Visibility

As of December 2025, Emmvee’s order book stands at 9.3 GW, providing strong medium-term revenue visibility.

-

6.3 GW scheduled for execution over the next 12–18 months

-

Major contract win:

-

4.5 GW TOPCon crystalline silicon cell order

-

Execution period: Dec 2025 to 2030

-

Long-duration contracts significantly de-risk future cash flows.

🏭 Backward Integration: Strengthening the Moat

Emmvee has fully paid for land for a 6 GW integrated solar module and cell manufacturing facility at Devanahalli, Bengaluru. Design and execution planning are currently underway.

Backward integration will:

-

Improve margin stability

-

Reduce dependency on imports

-

Enhance control over technology and quality

💰 Balance Sheet & Return Ratios: A Rare Combination

-

Net Debt / Equity: (-0.02x) → effectively a net cash company

-

Annualised ROCE (Q3 FY26): 36.5%

-

Annualised ROE (Q3 FY26): 49.9%

In a sector known for high leverage, Emmvee’s balance sheet strength stands out.

🧠 Management Commentary – What Matters to Investors

Management attributed the strong performance to:

-

Rapid capacity additions

-

Focus on TOPCon technology

-

Disciplined capital allocation

The company reiterated its confidence in executing expansion plans while maintaining balance sheet strength.

🔎 Business Snapshot

-

Second-largest pure-play integrated module & cell manufacturer in India

-

TOPCon cell capacity: 2.94 GW

-

Strategic technology partnership with Fraunhofer ISE

-

Manufacturing units concentrated within Karnataka (logistics advantage)

📈 Investor View: The FinanceBuz Take

Positives

-

Explosive revenue and profit growth

-

Industry-leading margins

-

Net cash balance sheet

-

Large, long-duration order book

Risks

-

Execution risk as capacity scales rapidly

-

Solar industry cyclicality and pricing pressure

Conclusion

Emmvee Photovoltaic Power Limited is emerging as a high-quality solar manufacturing compounder, combining scale, profitability, and financial discipline. If execution remains on track, the company is well-positioned to be a long-term beneficiary of India’s renewable energy push.

📌 This stock is worth close tracking by investors looking for high-growth opportunities in India’s clean energy manufacturing ecosystem.

Disclaimer: This article is for informational purposes only and should not be considered investment advice.